Frequently Asked Questions

Why child education solution ?

How it works?

What are the factors in calculating the SIP amount?

Who can invest?

What is the minimum investment amount?

Is there any lock-in period?

Where will the funds be invested?

The funds will be invested in Nippon India Equity Hybrid Fund (Number of Segregated Portfolios – 2).

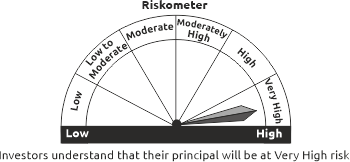

Nippon India Equity Hybrid Fund (Number of Segregated Portfolios – 2) is suitable for investors who are seeking*:

Long term capital growth.

Investment in equity and equity related instruments and fixed income instruments.

*Investors should consult their financial advisors

if in doubt about whether the product is suitable for them.

Why Nippon India Equity Hybrid Fund (Number of Segregated Portfolios – 2)?

Can I invest more whenever I have any surplus income or money?

Can I redeem before the goal tenure?

Are there any charges or expenses if I redeem before the goal tenure?

What will be the taxation implications?

Why child education solution ?

How it works?

What are the factors in calculating the SIP amount?

Who can invest?

What is the minimum investment amount?

Is there any lock-in period?

Where will the funds be invested?

The funds will be invested in Nippon India Equity Hybrid Fund (Number of Segregated Portfolios – 2).

|

Nippon India Equity Hybrid Fund (Number of Segregated Portfolios – 2) is suitable for investors who are seeking*: *Investors should consult their financial advisors if in doubt about whether the product is suitable for them. |

|